For many people, the difference between a retirement filled with enjoyment, fun and security and a retirement dominated by worry, concern and fear depends on a single factor: income. But there are a number of words that must be placed in front of the word “income” before you can get what you really need. Ample Income Lifetime Income Inflation-Adjusted Income Tax-Efficient Income And perhaps the most important one of all: Spendable Income Spendable income means what remains of your income after taxes that is available to spend on the things you need and want throughout retirement. Generally speaking, there are two ways you can try to increase spendable retirement income. One approach is to attempt to increase the growth rates or returns on your savings and investments. A one or two percent increase in return each year can make a big difference in the amount of income your portfolio can provide. Unfortunately, from a risk management perspective, we know that in order to get a boost in return we must either select financial instruments higher up on the risk vs. reward pyramid, meaning more risk of investment loss, or instruments higher up on the time vs. reward pyramid, meaning committing our money for longer terms or maturity dates. But for some, there may be another option that should at least be considered. If we can find a legal way to reduce the amount of taxes we must pay on our income, then we end up with a greater amount of net after-tax spendable income. For example, assume your savings along with your Social Security provides you with a total annual gross taxable income of $80,000, and that taxes consume 25 percent of that. You are left with $60,000. This is enough to meet your basic, essential living expenses necessary to keep a roof over your head, buy groceries, pay your medical bills and for other essentials. Unfortunately, little remains for vacations, to pay country club dues, buy gifts for the grandkids, go out to dinner or do the other things that might make life more enjoyable. Let’s say you would like an extra $4,000 a year to go on an ocean cruise or other trip. If you have savings of $400,000, one solution would be to figure out a way to increase the annual rate of return it generates by 1 percent ($400,000 X 1% = $4,000). If the rate of return currently generated on your savings equals six percent, you would have to figure out a way to boost the overall return to seven percent to generate the additional $4,000. And again, this will likely require that you either expose your savings to a greater risk of investment loss or commit your savings for longer periods of time. A possible alternative is to try to generate an additional $4,000 by reducing your tax rate from 25 percent to perhaps 20 percent. Now, instead of having a net after-tax income of $60,000 ($80,000 – 25%), you would have $64,000 ($80,000 – 20%). Your spendable income increases by $4,000. As long as you used a legal method to reduce your taxes, it potentially becomes a way of increasing your spendable income without increasing exposure to the risk of investment losses. From a risk management perspective, it doesn’t get much better than that. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable.

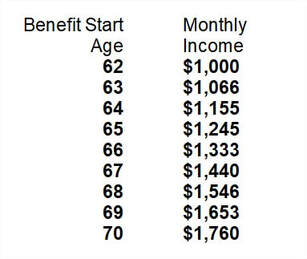

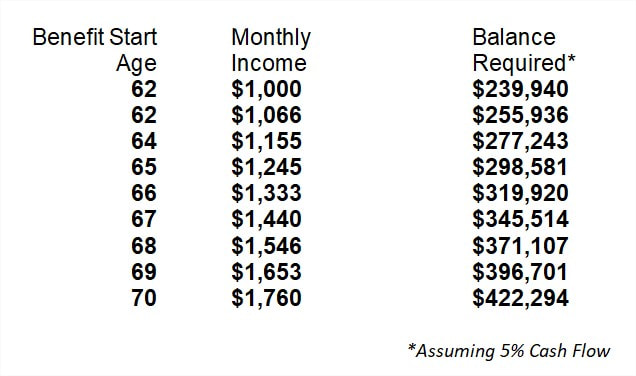

The benefit amount you will receive from Social Security will be based on your work and earnings history as well as the age at which you start your benefits. For example, assume that an individual born in 1952 had a work and earnings history that would generate a monthly benefit of $1,000 when started at the earliest possible age of 62. The following table shows how that benefit amount increases for each year that he delays the start of his benefit.  The longer you delay the start, the larger your benefit will be. Pensions and many income annuities are based on the same principle. Pick an early start age and your income amount will be less; delay the start age and you’ll receive a larger lifelong income. Like pensions and fixed income annuities, Social Security is not an investment vehicle. It is very specifically designed as an income vehicle for the purpose of providing you a lifetime income. However, it might be of interest to consider how large of a balance you would need to have in an investment account in order to generate the same income provided by Social Security. Assuming the investment “could” support a cash flow to you of five percent of the balance annually, the table below shows the approximate balances you would need in order to match the same Social Security income amounts referred to in the prior table.  When you look at it this way, you could say that if you did not have Social Security, you would need to accumulate an investment balance of $239,940 by age 62 in order to generate a monthly income of $1,000, assuming that investment vehicle would support a five percent cash flow. Or, by age 70, your investment vehicle would need a balance of $422,284 to support a monthly income of $1,760, assuming a five percent cash flow. One way to look at the difference between starting your Social Security benefit at age 70 and starting it at age 62 is that the extra $760 ($1,760 - $1,000) of monthly income you receive is like having an extra $182,354 ($422,294 - $239,940) in an investment account. Whether the strategy of starting a lower benefit early or the strategy of starting a larger benefit later appears best mathematically will depend on the assumptions you use: how long you expect to live, what rate of return you expect to earn on your investments, the level of future cost of living adjustments, and even the tax rates you assume you must pay. Because these assumptions — especially regarding how long we will live — can be highly inaccurate, the best we might do is to guess which strategy would be best. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable.

|

RSS Feed

RSS Feed

Services |

|