|

Regardless of where the bond is placed on this risk vs. reward pyramid, between the date it is first issued and the end of its term, investors can buy and sell these bonds just like any other investment. But the price at which any bond can be bought or sold will not necessarily be the same price as it was when it the bond was originally issued. This means that any investor who sells her bond before the end of its term must accept the risk that she could get back less than the amount she originally paid for the bond. The reason for this potential for loss is due to another form of risk commonly referred to as interest rate risk.  Interest rate risk is the potential that the value of a bond will go down as overall interest rates go up. To understand why, consider the following example. Suppose you have $1,000 in a bank CD that is maturing. The bank tells you that if you renew the CD for four more years, it will pay you interest on your money at the rate of three percent annually. You like the protection that FDIC insurance provides, but because you are concerned with the potential for inflation risk and the risk that you might outlive your savings, you decide to look for an alternative offering a higher rate. You find a bond that is issued by an institution you believe is so rock-solid that the potential risk of default is non-existent. The bond has a 20-year term and the issuer guarantees to pay you a higher rate of four percent annually. You like the interest rate offered, but you are a little concerned about the length of the bond term. This concern goes away when you are told that should you ever need your money, you always have the option of selling the bond at any time prior to the end of its term. You purchase the bond and are content earning your additional one percent interest, but only until a few years later when you see an advertisement in the newspaper showing that your former bank is now offering a four-year CD paying an even higher five percent interest. Now you are not so happy earning four percent on your bond. A simple solution might seem to be to sell your bond and deposit the proceeds in the CD that’s now paying a higher rate.

However, while it is true that the bond can be sold at any time, the potential problem is that there is no guarantee that anyone would purchase your bond for the same price you paid. In fact, if a potential buyer could just as easily deposit their money in a bank CD paying five percent interest, why would they ever purchase your bond that only pays four percent? What you will likely be forced to do in order to sell your bond is to reduce its price and take an investment loss. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable.

0 Comments

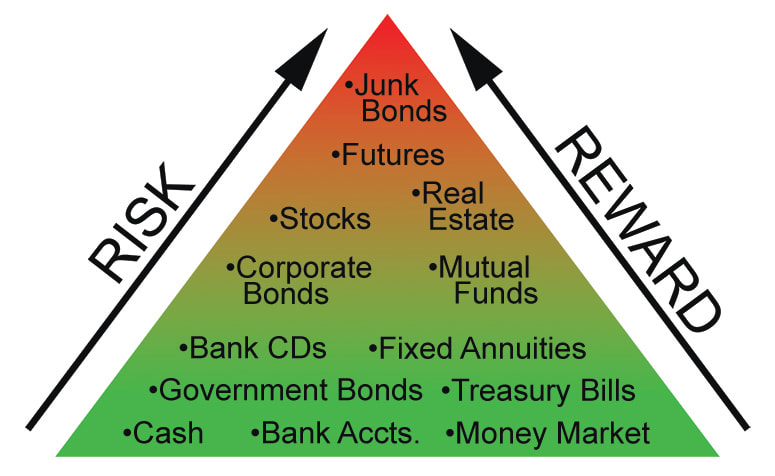

Because a bond entitles its owner to income and capital return, the strength and security of the institution borrowing the money is of prime importance. One risk that bond holders are exposed to is the risk that the institution defaults on the bond. This is the same risk that any lender faces. A bank attempts to assess how creditworthy a person is before lending that person money, because the bank must always be concerned that the borrower might default on the loan. When you invest in bonds, you are in effect taking on the role of the banker lending money. And as banks do, you must manage the risk that your borrower (the institution issuing the bond) won’t default. It is primarily due to this potential default risk that bonds have their own risk vs. reward pyramid.  At the bottom of this pyramid there is less risk of a default. Here, we find bonds issued by institutions believed to be the most secure. There are few more secure bonds than those issued by the U.S. Federal government. Because of this, you find these bonds at the very bottom of the pyramid. Higher up on the pyramid, you find bonds issued by large corporations: those that have been in business for a long time, with stellar financial strength and a long history of creditworthiness. And still higher on the pyramid, you find bonds issued by smaller, newer corporations with less of a track record. Higher still will be bonds issued by some corporations and perhaps even some municipalities that are facing financial difficulties. On the risk side, the idea is that as you move up the pyramid, there is a greater risk of default, because the bonds are issued by less and less creditworthy corporations and institutions. On the reward side, the interest rates you earn on these bonds also increases as you move up the pyramid. The more secure and creditworthy the bond issuer is, the less chance they will default, and the easier it is for them to attract purchasers of their bonds. The easier it is to attract a purchaser because of creditworthiness, the less interest the issuer will have to pay on their bonds. Again, U.S. Federal Government bonds are at the bottom of the pyramid, and the reason is both that the risk of default is so low and also that the reward they provide, or the interest they pay, is low as well. As you move up the pyramid, the risk of default increases, and because of it, the bond issuers have a more difficult time attracting purchasers. To get others to purchase their bonds, the bond issuers have to reward them for taking higher risk by providing a higher rate of interest paid. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable.

|

RSS Feed

RSS Feed

Services |

|