|

The risk of living too long, otherwise known as longevity risk, refers to the potential that a person might outlive his or her savings. Average life expectancy at age 65 is currently 19 years for males (i.e. a 65 year old is expected to live to age 84) and 22 years for females (i.e. a 65 year old is expected to live to age 87). But these are averages – about half the population is expected to live longer than this. Because it is impossible to accurately predict a person’s individual lifespan, it is not only difficult to manage longevity risk, it adds complexity to just about every aspect of retirement planning. For example, take Betty, a 65-year-old retired business owner with savings of $1 million. She, like most retirees, would like to know how much of this $1 million she could withdraw each year to not only meet her spending needs but at the same time reduce the risk of outliving her savings. The answer to this question will depend on many factors such as the anticipated growth rate of the money, its tax treatment, the impact of inflation and Betty’s probable lifespan, to name just a few. While it may be possible to make some fairly accurate estimates as to things like growth rates and taxation, how long a person will live is difficult if not impossible to come close to predicting. Of all factors, lifespan may in fact be the single most important one in trying to estimate how long your savings might last. To show why, let’s eliminate all of the other factors so that we can just focus on the impact of only lifespan.  To illustrate, assume that Betty’s $1,000,000 will not grow at all, no taxes will be due on this money and we are unconcerned about inflation.

Under these circumstances, we can simply divide Betty’s $1,000,000 by the number of years she is expected to live to determine how much she can withdraw each year. As previously stated, the average life expectancy for a female age 65 is age 87 or 22 more years. $1 million divided by 22 years equals $45,455 (annual income). But again, living to age 87 is only an average, and a fairly useless number for the purposes of planning considering that about half the females age 65 will live longer and about half will never make it to the average age of 87. If Betty believed that she would only make it to age 81 (16 more years) she could spend much more of her savings each year. $1 million divided by 16 years equals $62,500 (annual income). That’s a $17,045 increase in income each year. But what if she is wrong? What if she instead lives to an even older age of 93? Unless she wants to be exposed to the potential risk of being broke at age 81 and spending the final 12 years of her life in poverty, she’s forced to significantly reduce her spending. $1 million divided by 28 equals $35,714 (annual income). That’s $26,786 less income each year. One of the greatest fears shared by retirees is that one day they will be old and broke because they outlived their money. Because of this, it is not unusual to find that instead of enjoying retirement with travel, pursuing hobbies and buying gifts for grand kids, many people do without in order to reduce the risk of outliving their savings. If Betty shares this concern and because if it limits her withdrawals to only $35,714, but lives to age 75, she would have only spent $357,140 of her original $1 million. The $642,860 remaining at her death might be great for her heirs, but a tragedy if Betty’s limited spending had prevented her from living her remaining years doing the things she truly wanted to do. One of the surest and most effective ways to combat longevity risk is to have reliable, consistent, lifelong retirement income. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable.

0 Comments

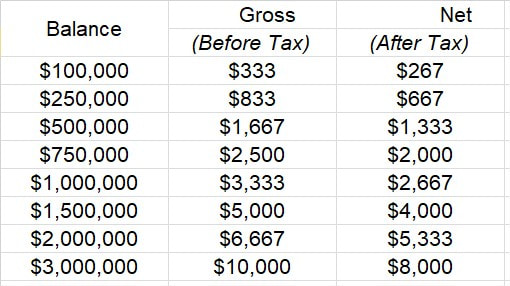

When participants start contributing to their 401(k)s, future taxes are generally of little concern. But as retirement approaches it becomes more apparent that taxes might present a significant problem, especially for those who fear that their tax rates might increase in the future. It’s not difficult to illustrate this as long as we remember that participants are only postponing the day when taxes must be paid on the money accumulating in their traditional 401(k)s, IRAs and other such retirement plans. When that day comes when you want to withdraw $50,000 for your retirement income, if the tax rate applied to the withdrawal is 20 percent, $10,000 will go to pay taxes. But if that tax rate has increased to 30 percent, the tax payment would go up to $15,000. Every dollar you pay in taxes is one less dollar available to pay your grocery, utilities, and insurance, let alone to fund travel, hobbies and the fun things we hope to do during retirement. Consider what this means in terms of actual income. For every $250,000 accumulated in your 401(k), IRA or other similar retirement plan, limiting withdrawals to a rate of four percent of the balance would provide a pre-tax income of $833 a month ($250,000 X 4% = $10,000 / 12 months). If 20 percent of this gross withdrawal goes to pay federal and state income taxes, you’re left with a spendable income of only $666 each month. A quarter of a million dollars is no small amount of money, and not easy to accumulate. But only $666 of spendable income each month doesn’t really go very far.  Safe Withdrawal Rate and TaxesMonthly Income Generated Assuming a 4% Withdrawal Rate and a 20% Effective Tax Rate  How much of a balance do you need in your 401(k) or IRA to provide what you would consider to be a large enough amount of after-tax spendable income?

Instead of consistently limiting withdrawals to four percent, many individuals might find that they are forced to periodically increase their withdrawals to meet some unexpected emergency. Or in a moment of weakness, they will pull more money out so they can go on a vacation, play more golf, or go out to dinner more frequently. Regardless of the reason, even a temporary increase in withdrawals, combined with the possibility of living a long life, can ultimately doom a person’s nest egg. While the impact may not be apparent for another decade or two, as baby boomers age and their retirement plan balances shrink due to the withdrawals they take from their do-it-yourself retirement plans. Ultimately it will be clear that the foundation supporting the retirement dreams of a great many people was less than solid. But, it won’t do you any good to allow yourself to become discouraged, even if you haven’t saved as much as you would have hoped and even if most of your savings is sitting in a 401(k), IRA or similar plan. While these plans present risks and challenges, so does everything else. The best solution, and the best way to plan your retirement so that you have the best chance of enjoying lifelong security and independence starts with a good risk management plan. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable. |

RSS Feed

RSS Feed

Services |

|