|

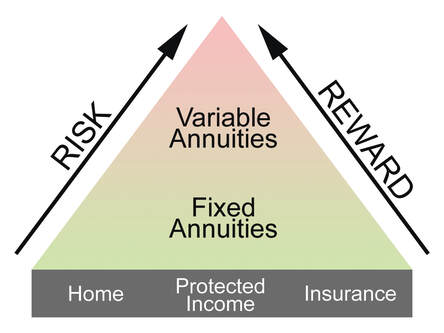

Other than Social Security or employer-provided pensions, annuities are the only financial instrument with the specific purpose of providing lifelong income. But before going further, it will be important to better define the type of annuity that will be discussed in this chapter for that purpose. There are many types of annuities, each designed with their own specific features and benefits. But generally speaking, all annuities can be placed in one of two different categories that are important to understand. There are fixed annuities and variable annuities. With fixed annuities, your money is never invested in stocks, mutual funds or instruments that have a risk of investment loss. The potential growth in the annuity is based on the crediting of an interest rate. The way that this interest rate is determined can vary widely between one fixed annuity and another. Variable annuities, on the other hand, provide the owner with options as to how the money is invested. Generally speaking, most variable annuities provide several choices that allow for all or a portion of the money to be invested in things that are very similar to stock market-type mutual funds that have a risk of investment losses.  Referring again to the risk vs. reward pyramid, it is appropriate to say that you would find fixed annuities located lower down on the pyramid because they provide protection against investment losses.

But you would also find them here because their reward, in terms of their growth potential, is also less. On the other hand, we would expect to find variable annuities much higher on the risk vs. reward pyramid, because they can be at greater risk of investment losses, but their reward in terms of their growth potential is higher as well. Each of these two basic forms of annuities can play a role in a person’s retirement planning, but it is important to realize that their role will likely be different. If we think of this in terms of the 100-minus age rule, or any method used to allocate a person’s retirement savings between instruments that are protected from investment loss and instruments that are at risk of investment loss, it can be said that it might be appropriate to use variable annuities for the at risk portion of the overall portfolio and fixed annuities for the protected portion of the portfolio. When an annuity is intended to be used to create a reliable, consistent, lifelong income, it might be better to consider a fixed annuity. The reason is that while variable annuities might have greater upside potential, their exposure to investment losses can undermine the reliability of their income. As you will see, the recommendations throughout this book are primarily to use a fixed annuity to provide just enough income to meet your basic essential living expenses. Once you know that your basic minimum income needs are met, you have more freedom to use securities, variable annuities or any other instrument you like to provide additional income. It is also important to understand that, generally speaking, there are two basic categories of fixed annuities. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable.

0 Comments

Under the Social Security Retirement Earnings Test (RET), the monthly benefit of a Social Security beneficiary who is below full retirement age (FRA) is reduced if he or she has earnings that exceed an annual threshold. Much has been written that suggests that this earnings test results in penalties or lost benefits. This is not entirely true, because if some of a recipient’s retirement benefits are withheld because of earnings, the recipient’s benefits will be increased starting at his or her full retirement age to take into account those months in which benefits were withheld. When a recipient is under his full retirement age, $1 will be held back from his benefit check for each $2 of earnings in excess of the specified limits of $18,240 (in 2020). This will change the year that the recipient reaches his full retirement age. That year, the recipient will have $1 held back from his benefit check for each $3 of earnings in excess of $48,600 (in 2020). This means that from the month of January until the month before the recipient attains full retirement age, the recipient is allowed to earn up to $48,600 (in 2020), and still receive his or her full Social Security retirement check.  The $48,600 (in 2020) applies if the recipient reaches full retirement age on or before the last day of the taxable year.

The $18,240 (in 2020) applies if the recipient does not reach full retirement age on or before the last day of the taxable year. After the month during which the recipient reaches his or her full retirement age, there is no longer any earnings limitation imposed. This means that a person can work beyond age 66 (for those born between 1943 and 1954), and regardless of the amount of the recipient’s earnings, he will receive the full Social Security retirement benefit. It is only earned income from wages and net income from self-employment that counts towards the specific earnings limit. Any unearned income from sources such as interest, dividends, distributions from IRAs, 401(k)s and other retirement plans, Roth IRAs, annuities or cash value loans from life insurance does not count towards the specified limits. Income earned by one spouse may or may not be included in the earnings test of the other spouse, depending on the circumstances. For example, an older spouse might be retired and receiving Social Security based on his own work and earnings record, while the younger spouse continues employment, and receives no Social Security benefit. In this case, even though they file a joint return, the younger spouse’s earnings would not be included in the older spouse’s earnings test. If, however, a retired spouse was collecting benefits, not based on her own work and earnings record but as a spouse, then her working husband’s earnings would be included in her earnings test. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable. Your advisor may have his or her own suggestions or methods to determine proper allocations to instruments on the risk vs. reward pyramid. One method that you might hear about or read about is commonly referred to as The Wall Street Rule of 100. While there are many reasons this “rule” has proven to be popular, a compelling one is its simplicity.  This rule dictates that the percentage of a person’s savings that is invested in equities should always equal 100-minus the person’s age.

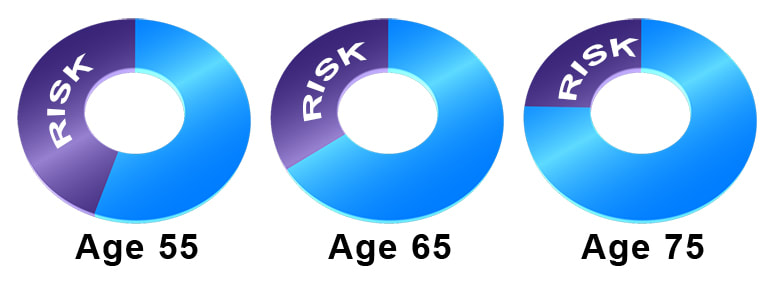

For example, a person who is age 55 should limit his percentage of stock market type investments to 45 percent of the total. At age 65, the portion invested in the stock market or items in a similar position on the risk vs. reward pyramid should be reduced to 35 percent of the total. And at age 75, there should be no more than 25 percent invested in stocks, mutual funds and the like. No allocation strategy is perfect, and there are those who criticize the 100-minus age rule as being far too simplistic, but generally speaking, the concept of reducing risk of investment losses as a person ages is sound. The reason, in part, is because as a person ages he or she may have less time to ride out the inevitable downturns in the stock market. Some advisors suggest that instead of 100-minus age, the rule should be modified so that it is 110 or some other higher number minus age. This would result in a larger allocation of the portfolio to equities and other instruments higher up on the risk vs. reward pyramid. The logic behind this position centers on the fact that today, people are living longer than they were when people first started using this allocation method, so the formula needs to be adjusted. There may be equally valid reasons for reducing the allocation to instruments at risk of investment loss if a person can’t tolerate volatility. A person should not feel compelled to use any specific allocation just because some rule or tactic says it is appropriate. The percentages used in any person’s actual retirement plan should be adjusted up or down based on individual circumstances and as accurate an assessment of a person’s true risk tolerance as is possible. For purposes of the discussion that follows, we will assume that a person and her advisor believe it is appropriate to follow the 100-minus age rule without any modification or adjustment. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable. There is a very definite and specific connection between risk and reward. Select financial instruments that provide more protection, or less risk of investment loss, and your reward will be less in terms of the potential return this money can earn. Take on greater risk that you could experience investment loss or that you will be forced to endure volatility, and you should expect to be rewarded with greater potential returns. Many people become frustrated or even get taken advantage of when they believe, or when an advisor tells them, that it is possible to break the connection between risk and reward. We all would like to find that perfect financial instrument that provides high returns with little or no risk and that would allow us to always get our hands on our money at any time it might be needed. You are at a party and a friend pulls you aside and tells you an amazing story. He has an investment advisor who has been making him a “ton of money” and doing it in a way in which there is no chance of any loss. Your friend started out by giving this advisor $10,000 to invest. Within months, he got a check back for $12,500. Of that, he again invested $10,000. And a few months, later he got another $12,500 check. “This works so well that I just sent him $70,000,” your friend announces.  Logic tells you that there must be something wrong with this.

But then, your friend tells you that his advisor is a highly respected financial expert who once served as the chair of the NASDAQ stock exchange.On top of that, he is so well-respected that dozens of banks and major charities trust him with their money. There are two things you can do at this point. Either plead with your friend to introduce you to his advisor, or pay closer attention to the unbreakable connection between risk and reward. If you did the first, your introduction would have been to a man by the name of Bernie, short for Bernard Madoff, otherwise known as inmate #61727-054 and currently residing at the Federal Correctional Complex, Butner in North Carolina. And with this introduction you would likely have eventually learned a very hard lesson. If you did the second and understood that anytime the potential investment reward seems too attractive it is because the risk is greater as well. Knowing this you would have recognized that a supposedly risk-free investment that earns a 50 percent return in a matter of months simply could not exist. It’s not that there aren’t investments that can deliver such high returns; it’s just that the only possible “investment” that could provide this kind of reward must also be very risky or an absolute fraud. So how did a slew of famous actors and actress, directors of movies, banks, hospitals and foundations get fooled? Every crook and Ponzi scheme operator in history knows the simple answer: these people wanted to believe. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable. |

RSS Feed

RSS Feed

Services |

|