|

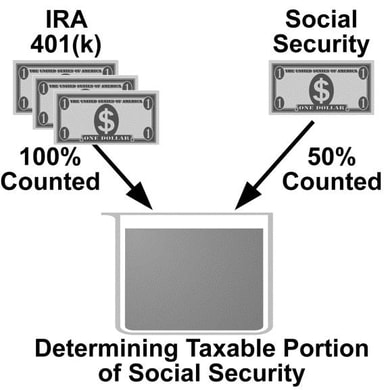

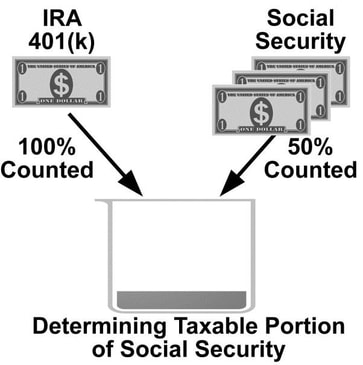

Social Security is subject to a unique tax treatment. Part of your benefit is taxed currently, and part is tax-free. But the portions of what is taxed and what is tax-free are rather fluid, and will depend in large part on the amount and most importantly, the sources of your income. To determine the taxable portion of your Social Security, the IRS takes all of your income and, figuratively speaking, puts it in a bucket to determine the total. The more that ends up in this bucket, the greater the percentage of your Social Security benefit that is taxable. But there is one very important thing to understand about these tax calculations: not all of your income necessarily goes into this bucket. If and how much of your income goes into the bucket is in large part based on the source of that income.  For example, 100 percent of the income you receive from your 401(K0, IRA or other tax-postponed retirement plan goes into the bucket, but only 50 percent of the income your receive from your Social Security goes into the bucket. Now think about that for a minute. If only 50 percent of the Social Security benefit you receive is included, doesn’t it stand to reason that your taxable income might reduce if a larger portion of your total income came from Social Security? To make this important point clearer, assume that we have two individuals. They both have the same total income.

Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable.

0 Comments

Mention the word “risk” to the three pigs from the children’s story and they see a scary vision of a wolf trying to blow down their house. Many people have a frightening view of risk, but it will most likely be one of investment losses destroying their retirement security. But even the smartest, brick-building pig would have met with tragedy if he only concerned himself with the sole risk of a huffing and puffing wolf. He needed strategies to protect himself from other risks, such as the wolf coming down his chimney. In much the same way, to keep our retirements secure, we must have a plan to protect ourselves from more than just the risk of volatile investments. Sometimes we can focus so much on reducing one form of risk that we can increase other, equally destructive risks.  A person determined to avoid the risk of investment losses could keep her life savings under her mattress. This would protect her savings from volatile investments, but what good does that do her if in the future she finds that she’s out of money because her savings never grew? During the market meltdown of 2008, many retirees, even those with well-diversified investment portfolios, saw the value of their holdings plunge by as much as 30 percent, 40 percent or more. Vowing to never again be exposed to this kind of risk, some of these people moved most or perhaps all of their savings into bank CDs and government-backed bonds. But if long-term interest rates paid on these protected instruments are less than the rate of inflation, these people may have destined themselves to a steady erosion of their wealth with consequences potentially as destructive as the risks of investment losses. Please do not misunderstand and assume that this article is in some way devoted to convincing risk-averse readers that they should have their money invested in the stock market. While in moderation, this might make sense for a great many readers, the point of raising these issues is more to help recognize that multiple risks must be managed during retirement, and that the steps we take to reduce one kind of risk might actually increase our exposure to another form of risk if we are not careful.  Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable.

|

RSS Feed

RSS Feed

Services |

|