|

Paying taxes is never fun. But once you stop working taxes can reduce what’s left to spend enjoying your retirement. Fortunately, there are some perfectly legal options that might allow you to put more of your retirement income in your pocket instead of Uncle Sam’s. Here are some things that might be worth discussing with your tax professional.  Will your taxes really be less in retirement? Many people expect their taxes will be less once they retire. But this assumption can lead to some nasty surprises. Here are four things that could lead to paying greater taxes than you might expect, once you stop working. · 100% of withdrawals from traditional IRAs, 401ks and other tax deferred retirement plans will be subject to income tax. · Up to 85% of Social Security retirement income could be subject to income tax. · Once a home mortgage is paid off, the tax reducing interest tax deduction is lost. · With huge deficits and growing popularity for increased government spending to fund universal health care, free college and environmental programs, tax rates could increase in the future. Forward vs. Backward Facing Planning Many people only take a backward-facing view of their taxes. As the April tax filing date approaches, they gather up their income statements and deductible expenses, take them to their tax preparer and hope for the best. A smarter approach might be to take a more forward-facing view of taxes. Especially when it comes to planning for retirement. This requires giving some thought to what your sources of income will be once you stop working. This can be important because different sources of income can result in a much different tax bill. Building future sources of income from financial instruments that qualify for reduced tax rates or where you might pay no taxes at all, could save you considerable money.  Tax diversification Many people use traditional IRAs and 401(k) plans to accumulate most, if not all their retirement funds. These accounts are popular because they can allow you to defer paying taxes on a portion of your income for decades. The problems this can create might only become apparent after you are retired, and it is time to start taking withdrawals from these accounts. Now 100% of this income will be subject to income tax. Not only that, for some people income from these sources could also cause a higher percentage of their Social Security to be subject to income tax. Building additional sources of income using accounts that are taxed differently can allow you to become better tax diversified. These sources can provide you with more options when it comes to deciding from which accounts you take withdrawals to fund your retirement. The time of your life

Retirement can be the time of your life, but it will take money. One of the biggest mistakes people make is to not consider the impact that taxes can have on their future income. Sure, you’ll need income to live the retirement you dream of, but the key is spendable income. How much of that income will be left after you pay taxes? Something important is about to happen Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable. Retirement could mean decades without a paycheck. Will you be prepared? How much will you need to save? Could taxes, inflation, rising health care expenses derail your plans for a secure and enjoyable retirement?  The approach advocated here is to build a strong foundation under your retirement by using an annuity to provide income sufficient to meet your basic living expenses. By focusing on devoting the minimum amount of savings to accomplish this objective, you should be able to determine precisely how much of your savings will remain to meet our other retirement objectives. This remaining money can be allocated to other financial instruments to provide potential growth and the additional income you’ll want for the more enjoyable things during your retirement. One possible benefit of taking this approach might be that you will have more confidence to spend some of your money on those enjoyable things, because you’ll know that your annuity, Social Security and other sources of protected income will be there to provide for your future expenses. Follow the steps below to arrive at the amount of income needed for this purpose. Once you know the amount of your basic living expenses that’s not covered by things like Social Security, you should be able to easily obtain annuity quotes from different insurance companies showing how much money would need to be allocated to the annuity in order to provide that needed income. Step #1 – Estimate your anticipated monthly living expenses during retirement. The approach that you want to take with this step is to try to envision your life during retirement and list the expenses that will be required to maintain your lifestyle. Next to each expense item you should place a check mark to indicate if this is an essential must have expense item as opposed to a want to have expense item. The purpose of listing these expenses is not to create a budget that you will use to dictate how you spend your money. Instead, the goal here is to come up with a total estimated amount of essential monthly expenses. Step #2 – Identify reliable and consistent income sources. In this step, you list the amounts and sources of protected income you expect to have available at retirement to help pay for those essential must have living expenses that you calculated in step #1. Protected income refers to income that is reliable, consistent and lifelong. And generally speaking, the types of income that meets this description are Social Security, employer-provided pension and income annuities. If you have other income sources that you believe are adequately protected, you can include them in the total, but the objective here should be to only include income that you are fairly certain you can count on regardless of future changes in the economy or financial markets. Rental income from property you own that has a long track record of being highly desirable and easy to keep rented might be an example of income you might want to include. If you have an employer-provided pension but are not yet retired and don’t know the amount of your projected pension income, you should be able to obtain an estimate from the employee benefits department at your work.

You’ll also want to obtain a current benefit statement from the Social Security Administration. There are step-by-step instructions in the back of this book showing how you can easily do this online. Step #3 – Obtain quotes from insurance companies. After you calculate your total essential must have expenses in step #1, and subtract your total protected income you determined in step #2, you will arrive at the amount of additional protected income you would want to have provided by an annuity. This will be your annuity income target. Now that you know this amount the correct path is to look for insurance companies that require you to pay the least amount of money in order to generate the targeted income. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable. While there are many reasons that a person would purchase an annuity, one major reason is to receive an income that will last as long as a person might live. To meet the qualification of a lifelong income annuity, the period of time that the income is paid is for at least for the life of the annuitant. Other income annuities might provide income for some specified period of time such as ten years, 20 years or even longer. While the annuitant might in fact not live longer than the specific period of time, there is no continuation of income if he or she does, unless the annuity has a payout period that is lifelong. So the basic difference can be stated simply: only a lifelong income annuity carries the specific promise to pay the annuitant a reliable, consistent income that lasts for at least as long as the annuitant lives, no matter how long that might be. To understand why fixed annuities can be a great choice for building your own personal pension, it is important to know that in at least one important way they are similar to your Social Security retirement benefits and many employer-sponsored pensions. Compared with selecting and managing stocks, bonds, mutual funds or just about any other financial instrument that might be used to generate future retirement income, annuities have little in common with the typical do-it-yourself retirement plans.  The responsibility for making sure that the annuity provides you with a reliable, consistent, lifelong income is shifted from you to the insurance company issuing your annuity. With many annuities, at the time of purchase you will know the exact minimum amount of income that will be provided at any future date when you might decide to start receiving that income. In other words, many annuities will provide a schedule that shows that at a minimum you will receive a specific amount of income based on a specific start date. The relationship between start date and amount of income is in some ways similar to Social Security in that the longer you delay the start of the annuity’s income, the greater the amount of the subsequent lifelong income you will receive. Instead of selecting and managing investments in the hope that they will provide lifelong income, with an annuity the insurance company issuing the annuity is promising you in advance the amount of lifelong income you will receive. That promise is backed by the full claims-paying ability of that insurance company. A joint life annuity protects a spouse by providing the continuation of a payout for the lifetime of both the annuitant and the surviving spouse. Lifetime income annuities with 10 years, 15 years or an even longer number of years of certain payments are another choice. These annuities provide for the continuation of the payout for a minimum certain number of years even if annuitant has died. But again, no matter how long the person lives, the income will continue. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable.

It’s not that 401(k) plans are necessarily bad, it is just important to understand that if you are counting on them to provide you with a reliable, consistent, lifelong retirement income you are going to have to do-it-yourself. When it comes to how the money in your plan is invested, it is your responsibility to try to pick the best options from those offered. If you want this money to provide an income, in a certain amount and for the rest of your life, it is you who must find a way to make that happen. Social Security and Employer Pensions mean: protected, lifelong income. 401(k) type plans mean: do-it-yourself investments that are either protected or unprotected depending you your choices. How much income they provide, and for how long is unprotected and based on your skill as an investor and money manager.  Unfortunately, when it comes to do-it-yourself investing, there is a great deal of evidence showing that many people haven’t done so well.

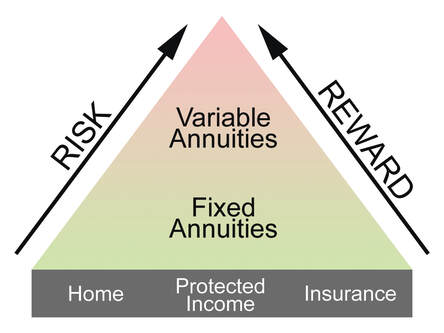

DALBAR Inc., a respected market research firm located in Boston, has been reporting the annual results of its Quantitative Analysis of Investor Behavior research for almost two decades, and the results always indicate that individual investors consistently underperform both the equities and bond markets by a wide margin. And this is true during both good and poor economic periods. Their report covering the 20-year period ending with the particularly devastating investment year of 2008 is even more disturbing, saying, “Equity fund investors lost 41.6% last year, compared with 37.7% for the S&P 500 Index.”[1] So during a year when the stock market was down 37.7 percent, the individual investor actually lost an even greater 41.6 percent. How does the individual investor do during years when the stock market performs better? DALBAR Inc., found that from 1986 to 2015 the average investor substantially underperformed compared to the S&P 500. Over 30 years, the S&P 500 returned 10.35%, but the average investor return was just 3.66%. What is responsible for this under performance? There is much evidence to support that the challenge of do-it-yourself investing is that our emotions can easily get in the way. The emotions of the typical individual investor cause him or her to buy and sell at the wrong time. But being a good investor is only half the battle. Once retired, the participant must now also figure out how to turn what she has accumulated in her do-it-yourself 401(k) type plan into reliable, consistent, lifelong income. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable. Other than Social Security or employer-provided pensions, annuities are the only financial instrument with the specific purpose of providing lifelong income. But before going further, it will be important to better define the type of annuity that will be discussed in this chapter for that purpose. There are many types of annuities, each designed with their own specific features and benefits. But generally speaking, all annuities can be placed in one of two different categories that are important to understand. There are fixed annuities and variable annuities. With fixed annuities, your money is never invested in stocks, mutual funds or instruments that have a risk of investment loss. The potential growth in the annuity is based on the crediting of an interest rate. The way that this interest rate is determined can vary widely between one fixed annuity and another. Variable annuities, on the other hand, provide the owner with options as to how the money is invested. Generally speaking, most variable annuities provide several choices that allow for all or a portion of the money to be invested in things that are very similar to stock market-type mutual funds that have a risk of investment losses.  Referring again to the risk vs. reward pyramid, it is appropriate to say that you would find fixed annuities located lower down on the pyramid because they provide protection against investment losses.

But you would also find them here because their reward, in terms of their growth potential, is also less. On the other hand, we would expect to find variable annuities much higher on the risk vs. reward pyramid, because they can be at greater risk of investment losses, but their reward in terms of their growth potential is higher as well. Each of these two basic forms of annuities can play a role in a person’s retirement planning, but it is important to realize that their role will likely be different. If we think of this in terms of the 100-minus age rule, or any method used to allocate a person’s retirement savings between instruments that are protected from investment loss and instruments that are at risk of investment loss, it can be said that it might be appropriate to use variable annuities for the at risk portion of the overall portfolio and fixed annuities for the protected portion of the portfolio. When an annuity is intended to be used to create a reliable, consistent, lifelong income, it might be better to consider a fixed annuity. The reason is that while variable annuities might have greater upside potential, their exposure to investment losses can undermine the reliability of their income. As you will see, the recommendations throughout this book are primarily to use a fixed annuity to provide just enough income to meet your basic essential living expenses. Once you know that your basic minimum income needs are met, you have more freedom to use securities, variable annuities or any other instrument you like to provide additional income. It is also important to understand that, generally speaking, there are two basic categories of fixed annuities. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable. Under the Social Security Retirement Earnings Test (RET), the monthly benefit of a Social Security beneficiary who is below full retirement age (FRA) is reduced if he or she has earnings that exceed an annual threshold. Much has been written that suggests that this earnings test results in penalties or lost benefits. This is not entirely true, because if some of a recipient’s retirement benefits are withheld because of earnings, the recipient’s benefits will be increased starting at his or her full retirement age to take into account those months in which benefits were withheld. When a recipient is under his full retirement age, $1 will be held back from his benefit check for each $2 of earnings in excess of the specified limits of $18,240 (in 2020). This will change the year that the recipient reaches his full retirement age. That year, the recipient will have $1 held back from his benefit check for each $3 of earnings in excess of $48,600 (in 2020). This means that from the month of January until the month before the recipient attains full retirement age, the recipient is allowed to earn up to $48,600 (in 2020), and still receive his or her full Social Security retirement check.  The $48,600 (in 2020) applies if the recipient reaches full retirement age on or before the last day of the taxable year.

The $18,240 (in 2020) applies if the recipient does not reach full retirement age on or before the last day of the taxable year. After the month during which the recipient reaches his or her full retirement age, there is no longer any earnings limitation imposed. This means that a person can work beyond age 66 (for those born between 1943 and 1954), and regardless of the amount of the recipient’s earnings, he will receive the full Social Security retirement benefit. It is only earned income from wages and net income from self-employment that counts towards the specific earnings limit. Any unearned income from sources such as interest, dividends, distributions from IRAs, 401(k)s and other retirement plans, Roth IRAs, annuities or cash value loans from life insurance does not count towards the specified limits. Income earned by one spouse may or may not be included in the earnings test of the other spouse, depending on the circumstances. For example, an older spouse might be retired and receiving Social Security based on his own work and earnings record, while the younger spouse continues employment, and receives no Social Security benefit. In this case, even though they file a joint return, the younger spouse’s earnings would not be included in the older spouse’s earnings test. If, however, a retired spouse was collecting benefits, not based on her own work and earnings record but as a spouse, then her working husband’s earnings would be included in her earnings test. Few things will be more important than your future retirement. And the way time flies, it will happen before you know it. We can help you plan for the inevitable. |

RSS Feed

RSS Feed

Services |

|